Every agentic commerce protocol was designed to reassure merchants. Merchants should read the fine print.

Every major agentic commerce protocol announced in the last six months, UCP, ACP, AP2, was designed to preserve something specific: the merchant stays the merchant of record.

That was not an accident. It was the concession that made the protocols politically viable. Google, Visa, Stripe, and Shopify understood that merchants would not integrate agent-accessible infrastructure if it meant ceding the customer relationship to the platform. So the architecture was built to let agents transact on behalf of consumers without the merchant losing record ownership. The brand stays the brand. The platform provides the rail.

This reassurance is technically accurate and strategically incomplete. Merchants who have taken the merchant of record language as the end of the analysis have answered the wrong question.

What merchants actually got

The merchant of record designation is not ceremonial. It carries real and specific protections.

Legal accountability stays with the brand. The customer's money flows to the merchant's payment infrastructure, not through the platform as an intermediary taking a cut before passing the remainder. The purchase confirmation carries the merchant's name. Returns, disputes, chargebacks, and warranty claims route through the merchant's systems. Fraud liability, tax collection, and consumer protection obligations all remain on the merchant's side of the transaction.

These protections matter. The history of platform commerce is full of examples where merchants who ceded merchant of record status found themselves progressively squeezed on margins, on data access, on customer relationship ownership as the platform gained leverage. The UCP and AP2 architectures were explicitly designed to avoid that outcome. The merchant record protection is real and worth preserving.

But preserving it requires understanding what it does and does not cover.

What merchants did not get

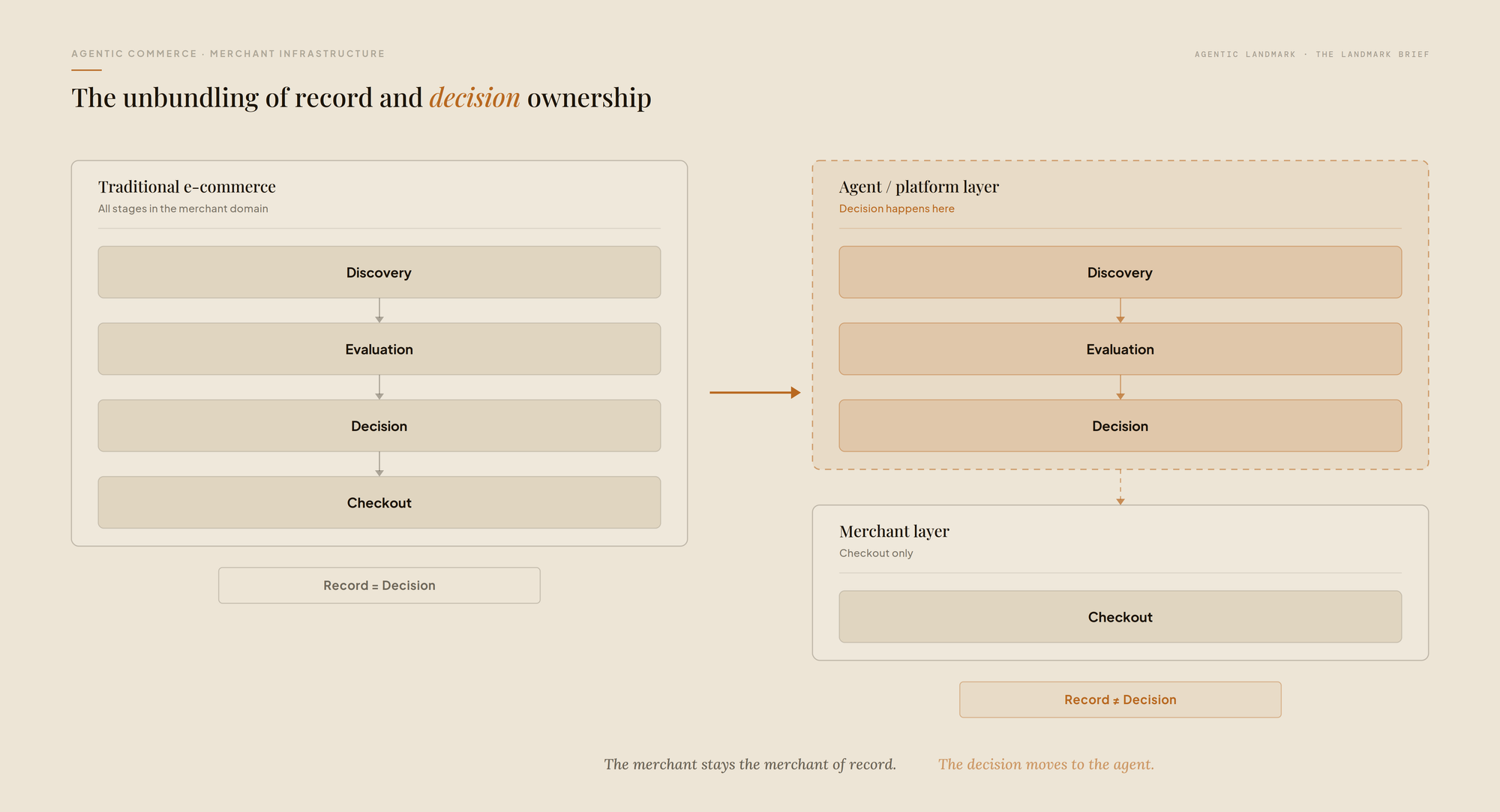

The merchant of record is not the merchant of decision.

In traditional e-commerce, the merchant controlled most of the purchase journey. Traffic arrived at the merchant's site. The merchant's search, navigation, and recommendation systems shaped what the consumer saw. The merchant's product pages, content, and trust signals influenced evaluation. The merchant's checkout design and promotional mechanics influenced conversion. Record ownership and decision influence were bundled together.

In agent-mediated commerce, they unbundle.

When a consumer configures a shopping agent with a price ceiling, preferred brands, and substitution rules, the discovery, comparison, price monitoring, compatibility checking, and purchase authorization all happen before any transaction fires inside the agent's evaluation logic, on the platform's infrastructure, before the merchant's site is ever visited. By the time the merchant's checkout processes the transaction, the decision was made elsewhere. The merchant executed it. They did not make it.

The merchant of record stays the merchant of record. The merchant of decision becomes whoever built the agent, designed the evaluation criteria, and owns the surface where the consumer's intent was formed and acted on.

This is Roger Dunn's observation from earlier this year: Google may be the merchant of decision for Universal Cart transactions while Gap, Nike, and Sephora remain the merchants of record. Both things can be simultaneously true, and they are not the same thing.

The loyalty and data problem

The strongest argument for maintaining merchant-controlled checkout is not the record ownership argument. It is the data and loyalty argument, and it is undernamed in most agentic commerce discussions.

Every transaction that flows through a merchant's own checkout generates signals that compound over time. Behavioral data tied to specific products, occasions, and purchase contexts. Loyalty program redemption events that reinforce the customer relationship. Post-purchase signals reviews, returns, repeat purchases that feed personalization and retention models. Email capture. First-party cookies. The raw material of lifetime customer value.

AP2 mandates route through Google Wallet. UCP transactions complete through the platform's payment infrastructure. When a transaction closes inside Google's Universal Cart, the merchant receives the order. They may not receive the full signal set that the same transaction would have generated inside their own checkout.

Every agent-mediated transaction that bypasses the merchant's checkout is a transaction where the data loop either does not close or closes more thinly. At low agent transaction volume, this gap is immaterial. As agent-mediated transactions grow toward the percentages that McKinsey and BCG are projecting, it becomes a compounding disadvantage. The merchants who built rich first-party data infrastructure from their own checkout are increasingly competing on signals that merchants whose transactions route through platform checkout infrastructure cannot accumulate at the same rate.

This is not a reason to reject UCP or AP2 integration. It is a reason to build loyalty and data capture into the agent-accessible checkout architecture from the start to ensure that the signals generated by agent transactions are as rich as those generated by human transactions, regardless of which checkout surface the transaction completed on.

The agent accessibility problem that most brands are missing

Maintaining a merchant-controlled checkout does not automatically make it agent-accessible. These are not the same investment, and most brands are treating them as if they were.

A checkout that requires browser navigation, clicking through a cart, filling a form, completing a payment page cannot be executed by an agent operating on a consumer's behalf without browser automation. A checkout that requires a logged-in user session to apply loyalty pricing is a checkout that an agent without cached session state cannot execute correctly. A checkout that calculates shipping in real time through a visual interface rather than through an API is a checkout that an agent cannot query before confirming a transaction.

The merchant of record status is preserved. The agent simply cannot use the checkout.

This is the most expensive misunderstanding in agentic commerce infrastructure planning right now. Brands are investing in protocol compliance, registering for UCP, integrating with AP2, and assuming that their existing checkout infrastructure is capable of executing the transactions that those protocols will route to them. It is not, in most cases. Protocol compliance is the agreement to accept agent-initiated transactions. Checkout agent accessibility is the infrastructure that actually executes them.

The build required to make a checkout agent-accessible is specific:

API-first checkout with endpoints that accept agent-initiated transaction parameters directly, without browser navigation. Real-time pricing and inventory APIs that an agent can query before confirming a purchase. Loyalty integration at the API layer so that loyalty pricing, earned rewards, and program benefits are accessible to agents operating on behalf of enrolled members. Protocol-specific authentication that proves agent authorization without requiring a live user session.

None of this is the same build as maintaining a best-in-class human checkout. The human checkout optimizes for visual conversion trust signals, progress indicators, payment method variety, and abandonment recovery. The agent checkout optimizes for programmatic reliability, API response speed, error handling, state management, and transaction confirmation. A brand can have an excellent human checkout and a completely inaccessible agent checkout simultaneously.

The three-build model

The merchants who navigate the next three years correctly are building three capabilities in parallel.

The human checkout for the Curator posture majority. These are the consumers who are still browsing, comparing, and deciding for themselves before they reach checkout. They represent the majority of the current market. They need the full human checkout experience, product pages, trust signals, seamless payment, and post-purchase confirmation. Underinvesting here because the agentic future is coming is a mistake. These consumers are the present revenue.

The agent-accessible checkout for the Scoper and Delegator posture consumers who have delegated execution to an agent. This checkout does not need to be visible or beautiful. It needs to be reliable, API-first, protocol-compliant, and capable of executing agent-initiated transactions with the same accuracy and completeness that human-initiated transactions achieve. Underinvesting here because it serves a small current minority is also a mistake. These consumers are the future revenue with the highest conversion probability.

The loyalty and data architecture that captures signals from both transaction paths. This is the layer that most brands are not thinking about yet. As agent transactions grow, first-party signal capture must extend into the agent transaction path. Loyalty redemption, behavioral signals, and post-purchase data need to flow from agent-initiated transactions as richly as they flow from human-initiated transactions. The brands that build this architecture now are the ones whose personalization and retention models will be richer in three years than competitors who let agent transactions flow through platform infrastructure without capturing the signals.

What the merchant of record actually means

The merchant of record designation is valuable. It is worth maintaining. The protocols that preserve it were designed with merchant interests in mind, and the protection is genuine.

But merchants who have read the merchant of record reassurance and concluded that the customer relationship is secure have answered the wrong question. Record ownership secures the transaction. Decision influence secures the relationship. In the era of agent-mediated commerce, the two are no longer bundled together by default.

The era of agentic commerce does not make merchant-controlled checkout less important. It makes the definition of controlled more specific: controlled for whom, accessible by what, capturing which signals, serving which checkout audiences simultaneously.

The merchants who answer those questions in their infrastructure planning now are the ones the next version of Google's launch list will include.