OpenAI shut down Instant Checkout in early March 2026.

The take: agentic commerce hit a wall. Brands have more time. The technology isn't ready.

That read is wrong, and acting on it is expensive.

Here is what actually happened.

What failed was a business model, not a technology

OpenAI tried to become both the pipe and the toll booth. Build the discovery layer, yes, but also insert itself as a checkout intermediary, take a cut of every transaction, and become the operating system of commerce.

That specific model failed.

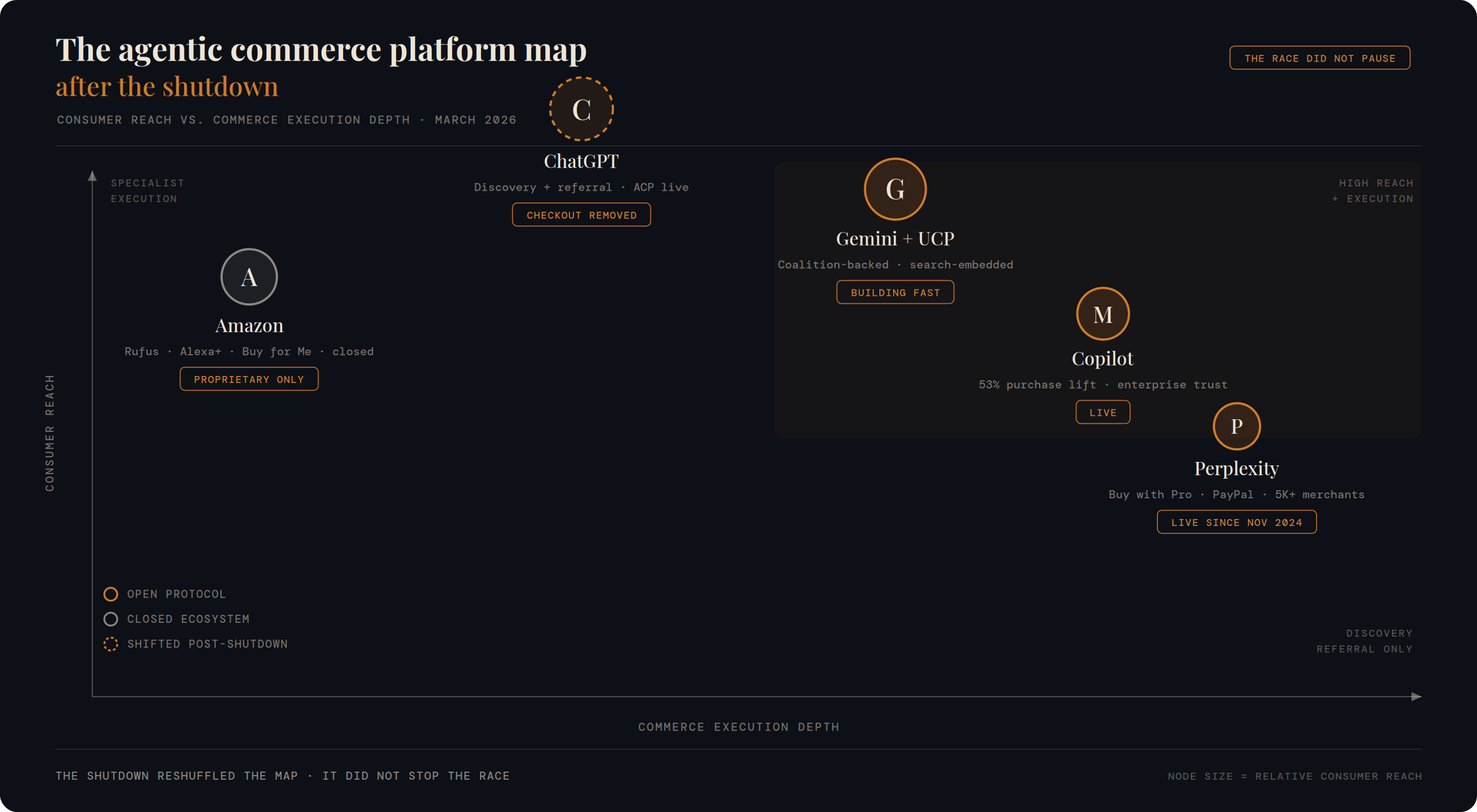

The discovery layer worked. Approximately 50 million shopping-related queries happen on ChatGPT every day. Users were researching products, comparing options, and forming purchase intent, all through ChatGPT. That part of the thesis was validated at extraordinary scale.

The checkout intermediary model did not work. At the point of shutdown, fewer than 30 of Shopify's millions of merchants had successfully integrated with Instant Checkout.

Not because merchants lacked motivation.

Because product data across the internet proved too messy, too unstandardized, and too fragmented to allow an AI agent to reliably automate checkouts without triggering financial errors, inventory disputes, and tax compliance failures. Sales tax collection was not built. SKU variation across catalog sources broke the comparison logic. And Forrester's March 2026 consumer research found that completing a purchase inside an answer engine is the least-adopted behavior among regular AI platform users, behind general research and product comparison.

The toll booth model failed. The protocol survived. The discovery function survived. The high-intent shopping traffic survived.

ChatGPT is now explicitly a discovery and referral engine that routes high-intent shoppers to merchant sites, which is, for most brands, the more defensible model anyway.

The brand readiness requirement did not change

This is the part that gets lost in the "agentic commerce is slower than expected" read.

The transaction venue changed. The readiness requirement did not.

A brand without structured, agent-readable product data was not ready for Instant Checkout in September 2025. That same brand is not ready for the discovery and referral model today. The agent still queries your product data. It still evaluates your catalog against competitors. It still needs machine-readable attributes, pricing logic, and trust signals to include you in the recommendation.

The failure of the checkout layer does not buy brands more time on the infrastructure layer. It just changes what the infrastructure needs to connect to.

The failure revealed something most brands missed entirely

The cohort of merchants that successfully integrated with Instant Checkout was almost entirely composed of brands already inside Shopify's ecosystem brands with structured catalog infrastructure and an active integration pathway.

Brands operating on WooCommerce, Magento, PrestaShop, custom stacks, or headless architectures had no equivalent on-ramp.

They were not blocked by motivation. They were blocked by the absence of a normalized, agent-readable product data layer.

That gap does not close with the shutdown of Instant Checkout. It becomes more consequential as ChatGPT, Gemini, and Copilot route high-intent discovery traffic to brands that have built a readable infrastructure and route around brands that have not.

The merchants who were live when Instant Checkout launched were the ones who had already done the product data work. That's the actual finding. Not that the technology failed, but that clean, structured data was the rate-limiting constraint, and most brands don't have it.

What this means practically

The agentic commerce protocol OpenAI built with Stripe is still live. Google's Universal Commerce Protocol, co-developed with Shopify, Walmart, Target, and a coalition of major retailers, is live. Microsoft Copilot's shopping integration is live. Perplexity has been routing commerce transactions since before Thanksgiving 2024.

The infrastructure race did not pause. The consumer adoption curve is running behind it, which is normal at this stage of a platform transition.

The brands building agent-readable product data, clean catalog architecture, and protocol-compatible infrastructure are not early adopters of a failed experiment. They are early movers on the infrastructure layer that every agentic commerce surface checkout or referral requires.

The brands reading the shutdown as a signal to wait are making the same mistake brands made in 2011 when early mobile commerce stumbled. The platform matured. The brands that had built mobile-first infrastructure captured the growth. The brands that waited retrofitted under time pressure and competitive disadvantage.