In March 2026, Boston Consulting Group published a scenario analysis on how AI agents will reshape retail commerce. Six Managing Directors and Partners built a four-scenario matrix. Named the imperatives that cut across every scenario. And told CEOs they could no longer afford to wait for clarity.

The most important sentence in the document is not one of the named scenarios. It is this:

"The marketing challenge isn't predicting which future will emerge, but building capabilities that are robust enough to succeed regardless of which futures unfold."

That sentence is the entire strategic case for agentic commerce infrastructure. Here is what it means in practice.

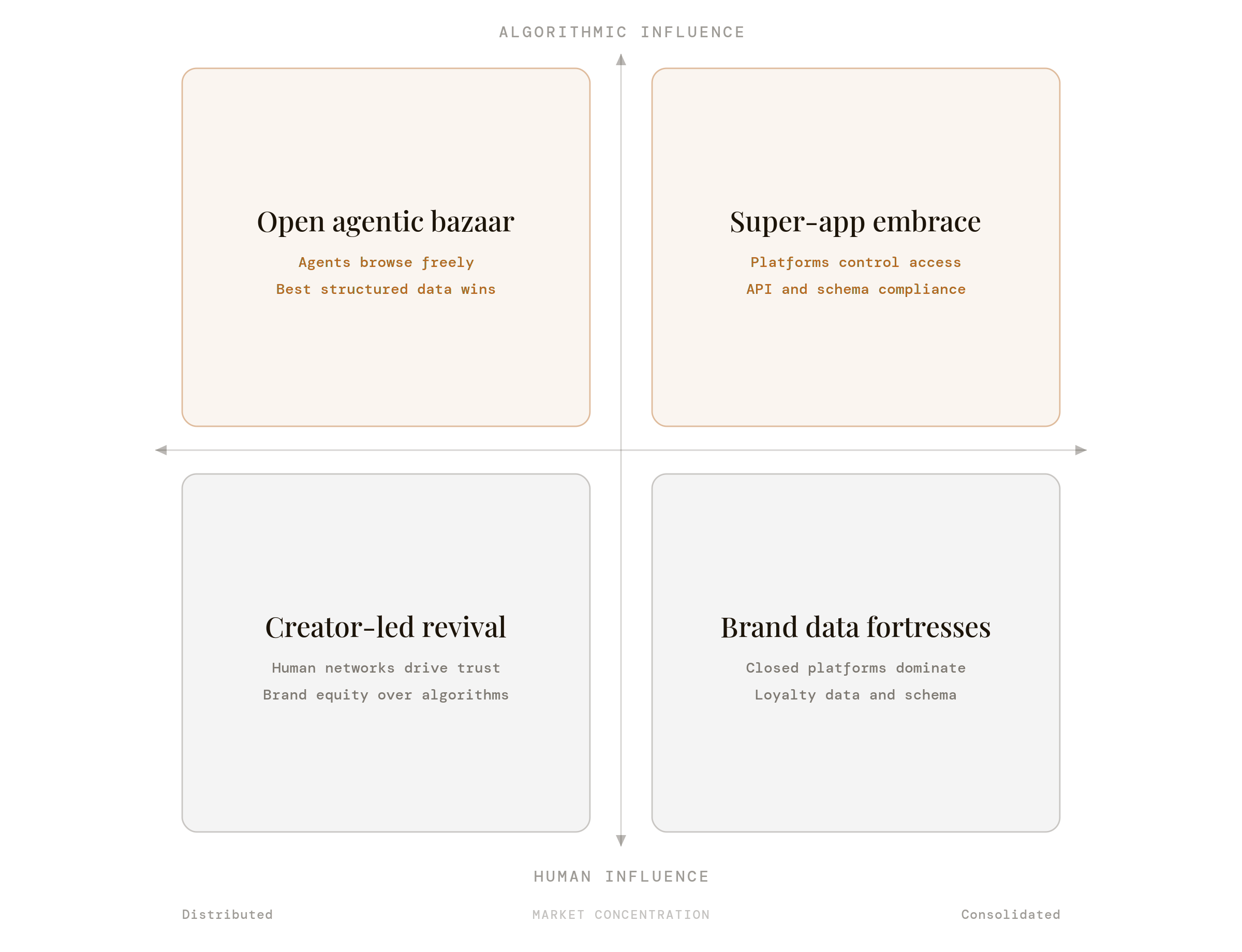

BCGs Four Scenarios

BCG structured their analysis around two variables: where will influence reside (algorithmic vs. human), and how will market power be concentrated (platforms vs. distributed agents).

The four combinations:

The Open Agentic Bazaar is distributed algorithmically. Agents browse freely across brands. Machine-readable product data and API accessibility determine who gets selected.

The Super-App Embrace consolidated, algorithmic. A handful of tech giants own the interface. Brands pay for access and optimize for each platform's proprietary logic.

Brand Resurgence Through Data Fortresses consolidated, human. A few large brands and retail platforms dominate. Loyalty architecture, closed ecosystem data, and proprietary agent engines are the moat.

Creator-Led Authenticity Revival distributed, human. Consumers trust creators over algorithms. Brand equity, community relationships, and transparent storytelling determine preference.

BCG is careful to say these are not mutually exclusive; some combination will coexist, and the dominant mix will vary by category and geography. What they cannot tell you is which combination will dominate, or when.

What Persists Across All Four

BCG named two imperatives that cut across every scenario: discoverability and desirability.

Discoverability is the ability to be found by agents, regardless of which system they operate in. The specific implementation differs by scenario. The underlying requirement that your product data is structured in a form agents can evaluate, rather than in prose and HTML spec tables, is the same in all four.

Desirability is a brand strength that survives algorithmic intermediation. BCG: "branding won't matter less; it will matter differently, but even more than it used to."

The data on both is pointed. BCG found only an 8 to 12 percent overlap between traditional search results and AI-generated answers. SEO and AEO are not the same channel. SEO captures bottom-funnel intent from humans already in buy mode. AEO influences the top and middle of the funnel, where agents build consideration sets before a human ever engages. A brand invisible at the AEO stage never appears in the shortlist that the consumer eventually reviews.

The Specific Gap Most Brands Are Missing

The brands capturing AI-referred traffic, which in live merchant data converts at 15.9% versus Google organic's 1.8%, have done something specific. They have expressed their product attributes as typed, machine-readable data rather than as prose copy.

An agent building a comparison matrix for a consumer cannot parse a paragraph into a comparison column. It can read a typed attribute directly. The difference between a brand that appears in an agent's shortlist and one that does not is often not product quality or price. It is whether the relevant attribute is in a Schema.org additionalProperty field or in a sentence.

Shopify merchants with agent-readable catalogs saw AI-sourced orders grow 15x in 12 months. The merchants not on that growth curve are running the same Shopify infrastructure with catalog data in the wrong format.

The Scenario-Robust Investment Case

BCG's most useful practical point is the reframing from forecast to preparedness.

Most brands are asking when agent-driven purchases will hit critical mass. BCG argues that it is the wrong question. The right question is how to build capabilities that work whether the market is 10% agent-driven or 90%.

Infrastructure investments compound. A brand that begins building structured data, entity records, and AEO content architecture in 2026 enters 2027 with 12 months of compounding in agent crawl indexes and citation patterns. A brand that starts in 2028 begins from zero while competing against brands that have had two years of compounding.

BCG on this: "CEOs cannot afford to wait any longer for clarity. The price of indecision compounds faster than the cost of making a mistake."

The Signal Worth Watching

BCG identifies a set of early signals that reveal which future is arriving: the growing share of purchase journeys that begin inside AI agents rather than search engines, whether AI assistants recommend brands by name or by specification, and how consumers respond to content they know was generated by machines.

The brands positioned to read those signals accurately are the ones that have already built the infrastructure that makes them legible to agents. Not because they predicted the right future. Because they invested in the one thing that matters in all four of them.

https://www.bcg.com/publications/2026/agentic-scenarios-every-marketer-must-prepare-for